ctcLink Accounting Manual | 40.50 Accounts Receivable

40.50 Accounts Receivable

2024-07-07

40.50.10 Definition

Receivables are defined as the amounts to be collected from private individuals, businesses, agencies, funds, or other governmental units.

Receivables are generally broken out by short-term (due within 12 months) or long-term (due in more than 12 months).

Depending on the government sector, receivables may be categorized by type of receivable (internal or external, governmental, or private or source).

40.50.20 Chart of Accounts

Receivables in the ctcLink chart of accounts are maintained with the account range 1010003 -1101999.

| Account | Description |

|---|---|

| 1010003-1019999 | Short-Term Receivables |

| 1010004-1010999 | Non-Student Short-Term Receivables |

| 1011004-1011999 | Student Accounts S-T Receivables |

| 1100003-1109999 | Long-Term Receivables |

| 1100004-1100999 | Non-Student Long-Term Receivables |

| 1101004-1101999 | Student Accounts L-T Receivables |

For accounts currently assigned and definitions for each account see CLAM 10.30.

Current defined receivable accounts

| Account | Description |

|---|---|

| 1010003 | Short-Term Receivables Budgetary |

| 1010004 | Non-Student Short-Term Rec Budgetary |

| 1010010 | AR Contra |

| 1010020 | Accounts Receivable ST |

| 1010030 | Int Receivable-Investments ST |

| 1010040 | Other Int Receivable ST |

| 1010050 | Unbilled Receivable ST |

| 1010060 | Other Receivable ST |

| 1010070 | Collections Receivable ST |

| 1010080 | AR Rebate Control |

| 1010090 | Conv-A/R |

| 1010100 | AR Control |

| 1010110 | Allow-Uncollectible AR ST |

| 1010115 | Allow-Uncoll AR ST Clearing |

| 1010120 | Allow-Uncollectible Loans ST |

| 1010130 | Allow-Uncollectible Other ST |

| 1010140 | Due From Other Funds VPA |

| 1010150 | Due From Fed Government ST |

| 1010160 | Due From Other Government ST |

| 1010170 | Due From Other Funds Intern ST |

| 1010180 | Due From Other St Agencies ST |

| 1010190 | Due From Other Funds Pool Cash |

| 1010200 | Due From State Allocation |

| 1010210 | Other Receivable Clearing |

| 1010220 | Third Party Errors |

| 1010230 | Travel Advances |

| 1010240 | Payroll Handwrites |

| 1010250 | Lease Receivable ST |

| 1011004 | Student Accounts Receivable Budgetary |

| 1011010 | SF Tuition Receivable (See CLAM 50.40) |

| 1011020 | SF Fees Receivable (See CLAM 50.40) |

| 1011029 | Non-Refund Receivable Clearing (See CLAM 50.40) |

| 1011030 | Fed Student Loans ST (See CLAM 50.40) |

| 1011040 | Fed Stdnt Loans Prnc Collected (See CLAM 50.40) |

| 1011050 | Fed Stdnt Loans Prnc Cncl (See CLAM 50.40) |

| 1011060 | Fed Stdnt Loans Int Cancelled (See CLAM 50.40) |

| 1011070 | Fed Student Loans Assigned (See CLAM 50.40) |

| 1011080 | Fed Student Loans Int Assigned (See CLAM 50.40) |

| 1011090 | 3rd Party Contract Clearing (See CLAM 50.40) |

| 1011100 | Payment Plan Receivable (See CLAM 50.40) |

| 1011105 | Payment Plan Clearing (See CLAM 50.40) |

| 1011110 | Student Loans Receivable ST (See CLAM 50.40) |

| 1011120 | Student R2T4 Loan Receivable (See CLAM 50.40) |

For accounts currently assigned and definitions for each account see CLAM 10.30.

40.50.30 Regulatory Requirements

The state of Washington directs colleges to promptly record (recognize) receivables when the asset or revenue recognition criteria have been met or the underlying accounting event has occurred, and the amount is determinable (measurable and available).

Under the modified accrual basis of accounting, revenues are recognized when susceptible to accrual; that is, when they become both measurable and available.

Measurable

Measurable means the amount of the transaction can be reasonably estimated.

Available

Available means collectible within the current period or soon enough thereafter to be used to pay liabilities of the current period. Primary revenues that are determined to be susceptible to accrual include federal grants-in-aid, and charges for services.

The state of Washington also requires receivables to be recorded in both the general ledger and subsidiary ledger.

Detailed receivable subsidiary ledgers

Detailed receivable subsidiary ledgers are to be established and maintained on an open item basis (i.e., an entry or entries in the subsidiary ledger for each outstanding amount due). The ctcLink accounts receivable module retains all historically data as well.

Colleges are required to establish a detailed subsidiary ledger in which the following specific information, at a minimum:

- Name of customer

- Account number of customer (or Unified Business Identifier number), if assigned

- Address of customer, if available

- Account control code (or equivalent indicator)

- Fund code (or equivalent indicator)

- Description of each outstanding charge and/or credit

- Invoice or document number

- Date of invoice or document

- Invoice due date (if different from date of invoice)

- Amount of each charge and/or credit

Certain requirements must be met to document Accounts Receivable.

| Requirement | Description |

|---|---|

| Sequentially numbered | Sequentially numbered billing documents (invoices) are to be used. |

| Invoices prepared | Invoices must be prepared and sent to customers. |

| Descriptive invoices | Invoices must contain a description of goods/services provided, dates provided, amount owed and a due date. |

| Receipts recorded daily | Receipts applicable to receivables must be recorded daily (should include payee/account number, amount received, invoice number, mode of payment and a payment reference number (e.g. check number). |

| Adjustments | Adjustments to receivables must be supported by a revised billing document or other appropriate documentation. The college must establish documented control to ensure our authorized adjustments occur. |

| Valuation | Valuation of receivables using the allowance method is to be made at least quarterly and at fiscal year-end to reflect the amount of receivable balances estimated to be collectible. |

| Track collections | A written record is to be kept, by account, on collection efforts. ctcLink AR module documentation the supports billing and past due will meet this requirement. |

| Write off uncollectible receivables |

For accounting and financial reporting purposes, write-offs of uncollectible receivables are to be made against the appropriate allowance accounts (accounts 1010110-1010130, 1010260 for short-term or accounts 1100020, 1100050, or 1101020 for long term receivables). Transaction documentation must include the name of the customer, the date of inception of the account, and the amount of the account being written-off. |

Subsidiary ledgers are to be balanced against the associated general ledger control accounts at least monthly.

40.50.40 Accounts Receivable Policies Required

Colleges are authorized to make a travel advance to defray some costs the traveler might incur while traveling on official college business. Colleges are required to establish written policies prescribing a reasonable amount for which advances can be provided.

Advances

- Shall not be provided more than 30 days in advance of travel

- May only be used to pay for reimbursable costs while on official business

- May not be used to purchase airfare

- May not be used to pay for use of privately owned vehicles

Travel advances are recorded to account 1010230 “Travel Advances” in the chartstring for which the applicable travel expense will be incurred.

If an employee fails to account for or repay an advance, the full unpaid amount is due immediately.

Colleges must charge interest of ten (10) percent per annum from date of default until paid.

The state has a prior lien against and shall withhold any and all amounts payable (including payroll) to the employee up to the amount of such travel advance and interest accrued.

Colleges should take advantage of the Uniform Commercial Code (UCC) provisions for dealing with NSF checks and other negotiable instructions. The UCC provisions found at RCW 62A.3-515 through 62A.3-525 are applicable.

Under the provisions of the UCC, colleges must send a notice of dishonor meeting statutory requirements contained in RCW 62A.3-520. After sending notice of dishonor under the provisions of the UCC agencies should:

- Collect a reasonable handling fee for each NSF check. Colleges must establish their handling fee by policy.

- After 15 days’ notice, charge interest at the rate of 12 percent per year.

Colleges must maintain adequate documentation of all deposit adjustments resulting in an amount due to the college.

Returned items should be re-deposited as soon as possible and if returned a second time, cash in bank should be adjusted and a receivable should be established.

For student accounts receivable see CLAM 50.40.

Colleges with more than $50,000 in past due receivables are required to prepare aging reports at least monthly. Aging reports are required to be reviewed by management and such review documented on the report.

Aging of receivables is a process used to assist in collection and/or write-off of delinquent accounts. Essentially, aging classifies receivables in terms of their delinquency status, i.e. 30, 60 or 90 days past due. The concept being that collection is more likely for less delinquent accounts than those held for longer periods.

Colleges must establish written procedures to ensure past due receivables are followed up promptly and in a manner that is cost-effective for the overall collection program.

These procedures are to provide for the full range of collection procedures to be used as appropriate, including issuance of statements and dunning letters, phone and personal interviews, filing of suits and liens, referral to private collection agencies or letter services, etc. as allowed by state law.

Colleges may use collection agencies for collecting outstanding debts as allowed by RCW 19.16.500 after reasonable efforts have been made to contact the debtor and provide notification the debt may be assigned to a collection agency. Colleges may charge a reasonable fee to the debtor for the services provided by the collection agency.

Colleges are only permitted to withhold transcripts from a student for outstanding debt for specific reasons as outlined in RCW 28B.10.293.

40.50.50 Interest Charges

Per RCW 43.17.240 colleges must charge 1% interest per month (12% annual rate) for all past due receivables unless certain conditions are met. This law does not apply to other governmental units.

40.50.60 Customer Accounts

Since the accounts receivable module is integrated with the general ledger, colleges must record all non-student receivables in the AR module except Third-Party Contractor accounts (see CLAM 50.60).

Please see the ctcLink Reference Center Accounts Receivables or the step-by-step processes for billings, receivables, and receipts.

For Student accounts see CLAM 50.40 and for Third-Party (External Org/Corporate) accounts see CLAM 50.60 in Student Financials.

For Student accounts see CLAM 50.40 and for Third-Party (External Org/Corporate) accounts see CLAM 50.60 in Student Financials.

For instructions on running an AR Ledger see CLAM 50.70.130 Account Analysis - Student and External Org Accounts Receivable Ledger.

40.50.70 Receivables Accounting

The community college system is a single state agency (agency number 6990) for purposes of budgeting and accounting in the state of Washington (even though each college district is also an agency). Because our system is a single state agency, receivables between districts and/or the State Board must be treated as interagency type (Intercollege Reimbursement) transactions to avoid duplication of expenditures and receivables.

Intercollege Reimbursements Due from Other State Agencies

By the end of this fiscal year all receivable balances between colleges/State Board must use account 1010180 Due from Other State Agencies with revenue account 4020120 Intercollege Reimbursement. This applies to all intercollege transactions.

The revenue account 4020120 is converted to a credit expenditure during the crosswalk to AFRS, effectively eliminating the duplication of expenditures on a college system-wide basis.

40.50.70.1.a OBIS

OBIS is the “Online Budgeting and Invoicing System” that allows access to grants administered by SBCTC. OBIS users access SBCTC online system for billing the State Board.

Billing the State Board through OBIS does not eliminate the need for the colleges to create invoices/receivables using either the Grants billing process or the accounts receivables module in ctcLink. OBIS eliminates the need to submit separate invoices

The community college system is a single state agency (agency number 6990) for purposes of budgeting and accounting in the state of Washington (even though each college district is also an agency).

Because each college is a state agency, receivables between districts and another state agency must be treated as interagency type transactions to avoid duplication of expenditures and receivables.

By the end of each fiscal year all receivable balances between colleges/State Board must use account 1010180 Due from Other State Agencies with the revenue account that aligns with the appropriate expenditure type:

| Account | Description |

|---|---|

| 4020020 | Interagency Reimbursement Salaries |

| 4020030 | Interagency Reimbursement Benefits |

| 4020040 | Shared Leave Reimbursement |

| 4020050 | Interagency Reimbursement Contracts |

| 4020060 | Interagency Reimbursement Goods/Service |

| 4020070 | Interagency Reimbursement Travel |

| 4020080 | Interagency Reimbursement Equipment |

| 4020090 | Interagency Reimbursement Comp Equip |

| 4020100 | Interagency Reimbursement Grants |

| 4020110 | Interagency Reimbursement Debt Svc |

The revenue accounts in this range are converted to a credit expenditure during the crosswalk to AFRS, effectively eliminating the duplication of expenditures on a state-wide basis.

Travel advance requests originate in the Expense module with the creation of a cash advance form in ctcLink. See Creating Cash Advances in the ctcLink Reference Center

This creates a debit to 1010230 Travel Advances and a credit 2000020 Expenses Control Liability in the chartstring configured in the employee travel profile. The liability is forwarded to AP for payment.

When the employee travels, expenses are netted against the advance eliminating the receivable. If the travel expenses claimed on the travel expense report are less than the advance, the balance of Travel Advances receivable remains until the amount is repaid.

Repayment normally occurs in Student Financials cashiering with a credit to the receivable (1010230) and a debit to cash in bank (1000070).

ctcLink has a process for unposted an NSF payment. This process reverses the original payment and restores the original receivable.

For a step-by-step process for un-posting an NSF payment see either

Colleges must also add the NSF charge (account 4030160) to the customer account. If the balance remains unpaid, interest must also be added using account 4030120.

40.50.70.5.a Aging Reports (Non-Student)

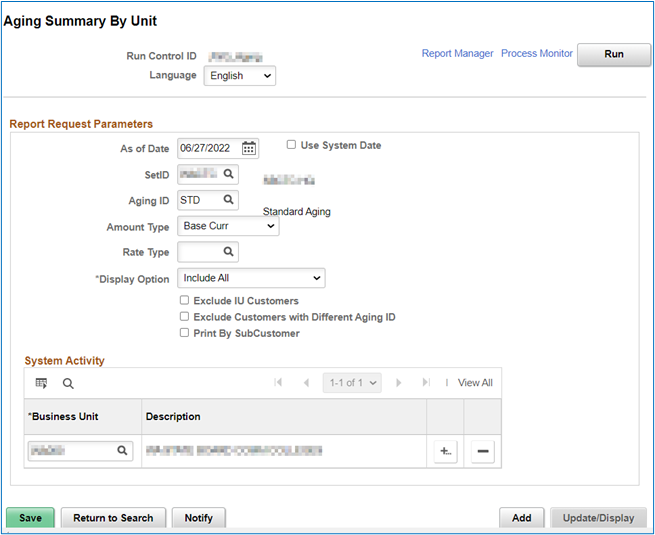

To run a customer (non-Student Financial) aging report in ctcLink go to:

NavBar > Menu > Accounts Receivable > Receivables Analysis > Aging > Aging Summary by Unit Report

Image 1: Aging Summary By Unit

The report provides aging for all accounts due more than 30 days:

Image 2: Aging Summary for All Accounts Due More than 30 Days

With totals by aging groups:

Image 3: Aging Summary by Aging Group

For instructions on running the report see Running the Aging Summary by Unit Report in the ctcLink Reference Center.

40.50.70.5.b Aging Reports (Student & Third-Party)

An aging report for student and third-party accounts is available in the Student Financials module of Campus Solutions. Example in section 50.70.130.

40.50.70.5.c Aging Reports (Combined)

An aging report that includes customer, student and third-party accounts is currently under development. This section will be updated when the report is available.

The amount determined to be collectible should be reflected on the financial statements as accounts receivable. Therefore, the amount determined uncollectible must be noted and recorded as estimated uncollectible, an offset to the receivable balance.

Estimates of total uncollectible receivables, using the allowance method, should be made at least quarterly and at fiscal year-end in the General Ledger to reflect the amount of receivable balances estimated to be collectible.

Governmental Funds

| Fund | Class | Dept | Method | Acct DR | Acct CR |

|---|---|---|---|---|---|

| Local Operating Fund | ccc | ddddd | Journal | (1) | (2) |

- Use the revenue account used to record the receivable

- Short-Term AR Allowance Accounts: 1010110 - 1010130, 1010260

Long-Term AR Allowance Accounts: 1100020, 1100050, or 1101020

Proprietary Funds

| Fund | Class | Dept | Method | Acct DR | Acct CR |

|---|---|---|---|---|---|

| Local Proprietary Fund | ccc | ddddd | Journal | 5081270 | (1) |

- Short-Term AR Allowance Accounts: 1010110 - 1010130, 1010260

Long-Term AR Allowance Accounts: 1100020, 1100050, or 1101020

A write-off is the elimination of uncollectible accounts receivable in the college accounting records. An accounts receivable balance represents an amount due to the college. If the individual/entity is unable to fulfill the obligation, the outstanding balance should be written off after collection attempts have occurred.

This only means the debt is no longer included in the college’s account receivables. If the individual/entity wishes to use the college services in the future, the written-off accounts receivable should be restored.

College staff must be aware of all legal limitations and/or requirements for providing or refusing to provide services to individuals/entities with uncollected receivables.

The write-off of uncollectible receivables must be subject to management review using procedures developed by the college in cooperation with the Attorney General’s Office.

This process assumes the college has previously recorded the above allowance entry since the process described below reduces the specific allowance account balance.

Governmental and Proprietary Funds

| Fund | Class | Dept | Method | Acct DR | Acct CR |

|---|---|---|---|---|---|

| Local Fund | ccc | ddddd | Accts Rec | (1) | (2) |

- Short-Term Receivables Allowance Accounts: 1010110-1010130, 1010260

Long-Term Receivables Allowance Accounts: 1100020, 1100050, or 1101020 - Use the original receivable account used to record the receivable.

In the event an insufficient balance exists in the allowance account, the college must reverse the original transaction (per state accounting rules).

Governmental and Proprietary Funds

| Fund | Class | Dept | Method | Acct DR | Acct CR |

|---|---|---|---|---|---|

| Local Fund | ccc | ddddd | Accts Rec | (1) | (2) |

- Original Revenue Account

- Original Receivable Account

See the step-by-step process for Non-Student Accounts in Writing an Item Off at the ctcLink Reference Center.

For write-off of Student and Third-Party accounts see CLAM 50.20 Student Financials.

40.40.70 Useful Queries << 40.50.70 >> 40.55 Liabilities